Prosperity Partners Blog

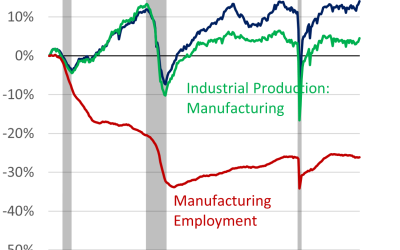

Manufacturing in Crisis

The Federal Reserve held its key rate, the fed funds rate, at 4.25 – 4.50% as expected. But Fed officials downgraded the economic outlook for 2025 and raised its forecast for inflation (again) in its quarterly Summary of Economic Projections.

Elevated Uncertainty, ‘Transitory’ Makes a Comeback

The Federal Reserve held its key rate, the fed funds rate, at 4.25 – 4.50% as expected. But Fed officials downgraded the economic outlook for 2025 and raised its forecast for inflation (again) in its quarterly Summary of Economic Projections.

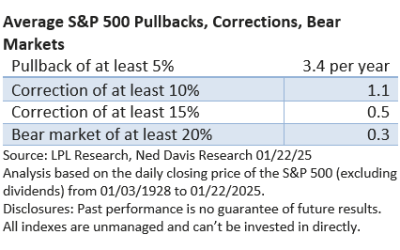

Entering a Market Correction

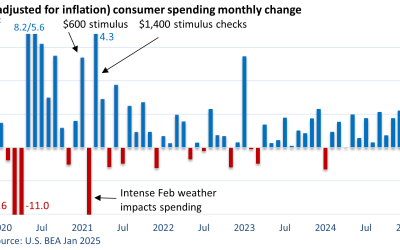

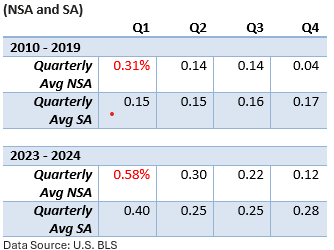

The February Consumer Price Index came in softer than expected, rising 0.2%, according to the U.S. BLS. The core CPI, which excludes food and energy, also rose 0.2%. The core CPI slowed to an annual rate of 3.1% from 3.3% in January. February’s rate was the slowest since early 2021.

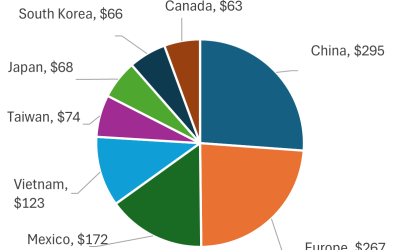

Tariffs On, Tariffs Off, Tariffs Back On (Sort of)

There are times when the economic data is strong, and when considered together, the economic reports surpass expectations. Such cycles run their course, and the economic reports turn softer. That overperform/underperform cycle can repeat itself multiple times during an economic expansion until the economy finally rolls over, and we land in a recession.

A Whiff of Uncertainty

There are times when the economic data is strong, and when considered together, the economic reports surpass expectations. Such cycles run their course, and the economic reports turn softer. That overperform/underperform cycle can repeat itself multiple times during an economic expansion until the economy finally rolls over, and we land in a recession.

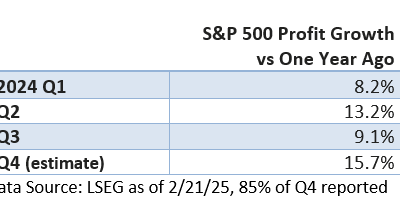

Earnings Impress

The U.S. Bureau of Economic Analysis (BEA) reported that Gross Domestic Product (GDP) expanded at an annual pace of 2.8% in Q3, which was down from 3.0% in Q2.

Explaining Away a Hot Inflation Report

The U.S. Bureau of Economic Analysis (BEA) reported that Gross Domestic Product (GDP) expanded at an annual pace of 2.8% in Q3, which was down from 3.0% in Q2.

Tariff Threat in Play

The U.S. Bureau of Economic Analysis (BEA) reported that Gross Domestic Product (GDP) expanded at an annual pace of 2.8% in Q3, which was down from 3.0% in Q2.

The Consumer Bolsters GDP

The U.S. Bureau of Economic Analysis (BEA) reported that Gross Domestic Product (GDP) expanded at an annual pace of 2.8% in Q3, which was down from 3.0% in Q2.

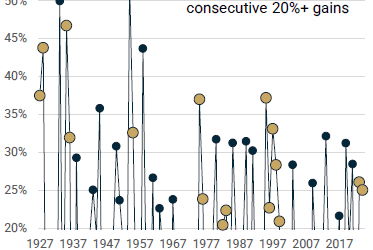

2024 Market Summary and Financial Forcast

Best Two Years in a Quarter-Century. In late 2022, a new bull market emerged from the ashes of a nine-month bear market, leading to 2023’s impressive rise of over 26% for the closely followed S&P 500 Index, according to S&P Global (including dividends reinvested).

Housing’s Worst Year in Nearly 30 Years

The U.S. Bureau of Economic Analysis (BEA) reported that Gross Domestic Product (GDP) expanded at an annual pace of 2.8% in Q3, which was down from 3.0% in Q2.

Despair to Jubilation and Beyond

The U.S. Bureau of Economic Analysis (BEA) reported that Gross Domestic Product (GDP) expanded at an annual pace of 2.8% in Q3, which was down from 3.0% in Q2.