Prosperity Partners Blog

The Road to Lower Inflation Takes a Detour

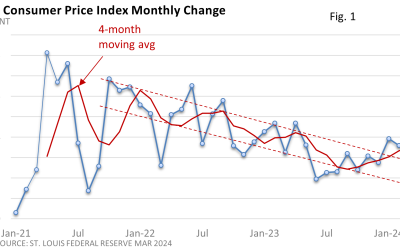

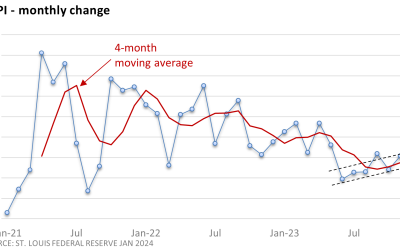

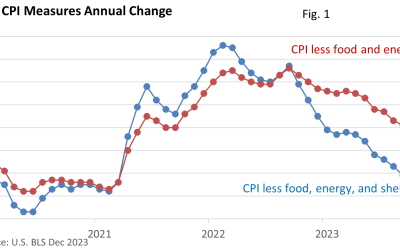

The rate of inflation is accelerating. That’s not how we hoped to start this week’s Insights. Take a moment and review Figure 1. The 4-month moving average has broken out of its long-term downward trend (red-dashed lines). On a monthly basis, prices bottomed in June and began to gradually turn higher. The upward trajectory picked up in January.

No Matter How You Slice It and Dice It…

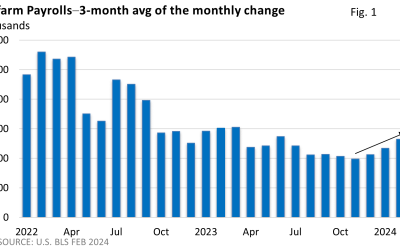

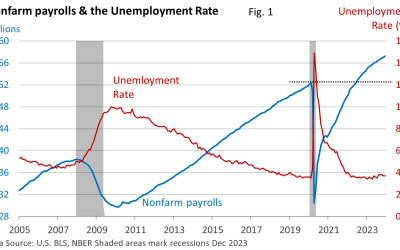

The latest employment numbers from the U.S. Bureau of Labor Statistics (BLS) point to a robust job market. On Friday, the U.S. BLS reported that nonfarm payrolls rose 303,000 in March, well ahead of expectations. It’s not simply March; growth has been above 250,000 for four months running.

Last Year’s Rally Spills into 2024

Stocks turned in a surprisingly strong 2023, and momentum has yet to slow in 2024 as last year’s rally remains in high gear. According to Dow Jones Market Data published by MarketWatch, the S&P 500 Index set 22 all-time closing highs this year. Likewise, the Dow notched 17 closing records, and the Nasdaq Composite recorded four new closing highs.

The Fed – Dovish as She Goes

The Federal Reserve held its benchmark rate, the fed funds rate, at 5.25 – 5.50% last week. That wasn’t a surprise. Let’s look at three important takeaways from the meeting that drove the Dow, the S&P 500 Index, and the Nasdaq to new closing highs on Wednesday and Thursday (MarketWatch data).

Are We There Yet

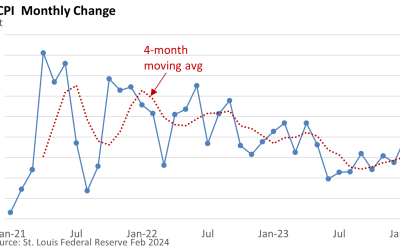

The road to price stability has been long and arduous. Inflation doesn’t just impact investors. It impacts everyone, from shoppers to travelers to those on a fixed income. February’s Consumer Price Index (CPI) marks the second straight month of stronger-than-expected inflation.

A Clear as Mud Jobs Report

On Friday, the U.S. Bureau of Labor Statistics (BLS) reported that employers added 275,000 net new jobs in February. The hiring boom continues, right? Well, it’s not quite that simple. Let’s dive in. January’s red-hot increase of 353,000 was revised lower to a still-strong 229,000. But that’s an unusually large downward revision.

Waiting… and Waiting for the Other Shoe to Drop

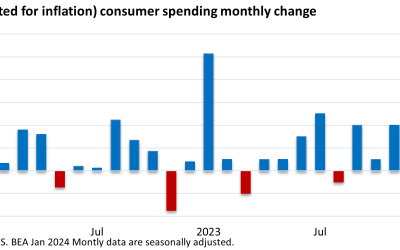

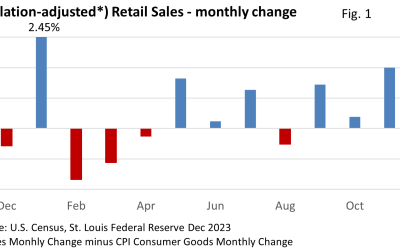

What is consumer spending? Loosely defined, consumer spending is the ‘stuff’ we buy. It is the goods and services we purchase. It is groceries, clothes, entertainment, health care, auto repair, insurance, appliances, utilities, wireless service, and much more.

Price Check

The road to price stability was never expected to be a straight line. The latest numbers show that the road isn’t even paved. Investors hit an unexpected pothole after the U.S. Bureau of Labor Statistics (BLS) reported January’s Consumer Price Index (CPI).

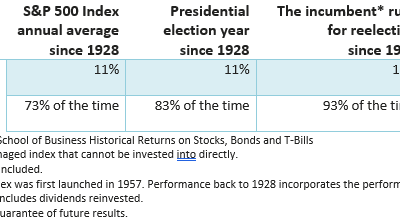

There is an Election This Year

Last week, we examined the relationship between interest rates and stocks. This week, we will analyze market performance during presidential election years. So, what might we expect based on historical returns during a presidential election year?

Waiting on the Long Awaited Soft Landing

Economists have been warning for quite some time that Fed rate hikes will slow economic growth. Whether it results in a soft landing, which is the preferred outcome for investors, or a hard landing (recession), the rate hikes would be expected to blunt economic activity, at least to some degree.

To Measure Inflation, Let Me Count the Ways

Investors eagerly anticipate the government’s monthly release of the CPI (Consumer Price Index). Why? Inflation affects everyone, and investors are no exception. The Federal Reserve’s efforts to curb inflation led to a bear market in 2022. However, fewer interest rate hikes in 2023 and a more lenient stance by the Fed contributed to the market’s recovery in 2023.

Steady Freddie Job Growth

The U.S. Bureau of Labor Statistics (BLS) reported that nonfarm payrolls rose by 216,000 in December, while October and November were revised down by a total of 71,000. The unemployment rate held steady at 3.7% in December.